Advancing South India’s Global Agenda

Cracks in the Cartel: Venkatakrishnan Asuri

BackCracks in the Cartel: Venkatakrishnan Asuri

Cracks in the Cartel

Author: Venkatakrishnan Asuri

Introduction

The United Arab Emirates’ decision to exit the OPEC grouping[1] has led to reverberations across commodity markets. The timing of the announcement is particularly interesting, coinciding with the ongoing GCC Summit in Jeddah. The exit is not without precedent: countries such as Ecuador, Angola, and notably Qatar[2] have withdrawn from the “oil cartel” in earlier years. This decision comes at a crucial timing, following weeks of missile and drone strikes by OPEC member Iran, alongside the blockade of the Strait of Hormuz putting pressure on the Emiratis’ economy. In this article, I shall discuss the several aspects of this move.

Scratching the Surface

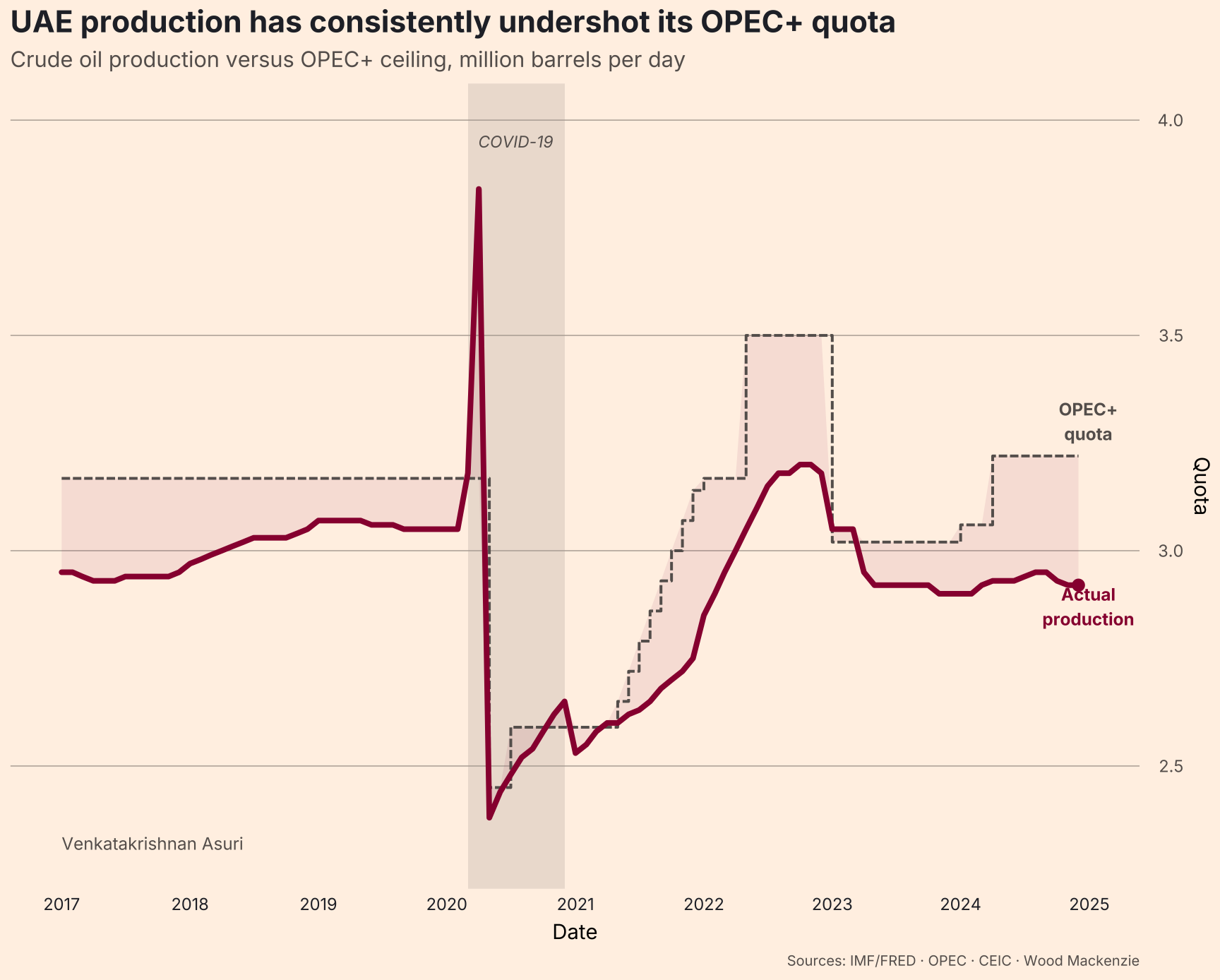

To start with, the conventional role of the OPEC has been one of a market stabiliser, by managing the price by controlling the supply of oil. Firstly, the UAE leadership’s decision to exit can be underlined by their frustration with OPEC’s production quotas and an economy less dependent on oil revenues, in comparison to other member states. To put this in perspective, UAE’s allowed production of ~3.2 mb/d remains well below its total capacity of ~4.9 mb/d[3]. They have been investing heavily to increase its production capacity to around 5 mb/d by 2027, having already invested $150 billion[4]. Clearly, the compliance with production quotas had become economically irrational for the UAE, with price management becoming less important than liquidity generation and market share. The exit also follows a time-bound logic: the perceived closing window for robust fossil fuel demand is projected to narrow by 2040[5], and they appear intent on monetising the oil revenues and reinvesting them into post-oil sectors.

Is it Shakika?

The most notable relationship in the GCC remains the Saudi-UAE one, which has moved through several phases in its past. While the Saudis use the word shakika (brotherhood) while referring to the Emiratis, it does not reflect the real nature of the relationship. There are two components to the divergence in their relationship - economic and strategic.

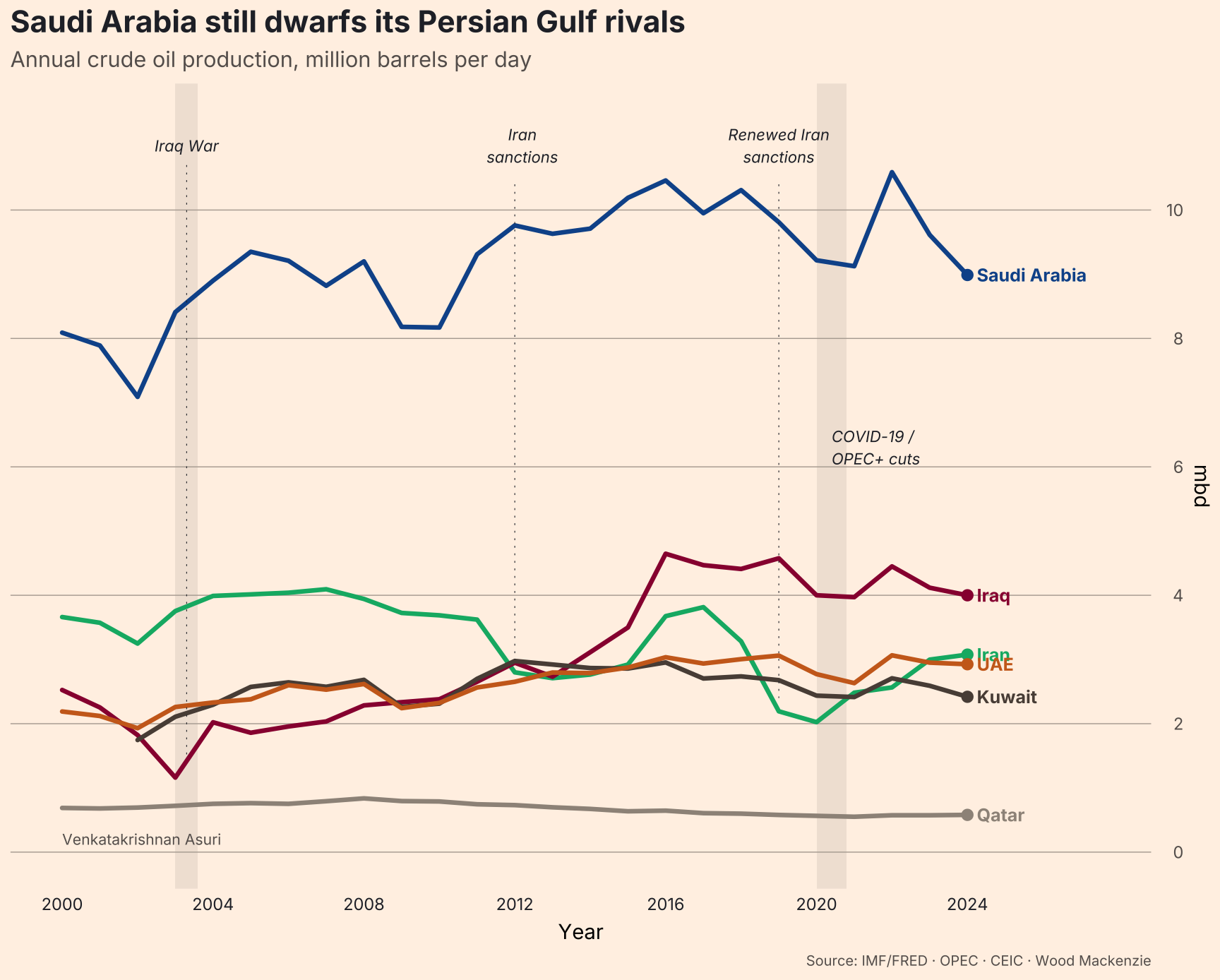

On the question of economic divergence, Saudi Arabia’s IMF-estimated fiscal break-even is at $78-85/barrel[6], rising to $111/barrel if Public Investment Fund (PIF) spending is included[7]. In contrast, UAE’s break-even hovers around $50/barrel[8]. This asymmetry in fiscal dependence on oil has exaggerated differences over pricing, with the Saudis favouring higher prices to sustain its Vision 2030 agenda. Unlike Saudi Arabia, which continues to defend prices through coordinated supply cuts, the UAE has substantial spare capacity that it plans to unlock from May 2026.

Despite public rhetoric, the UAE views Riyadh as a major security concern, second only to Tehran. The differences stem from a variety of reasons ranging from the post-2004 Emirati leadership’s skepticism of Wahhabism to the two players backing opposite sides in civil wars in Yemen and Sudan. The war in Iran was the last domino, with the Saudi reluctance to join the Abraham Accords exposing the lack of collective security within an increasingly fragile GCC. Divergent visions of the future, including around the post-oil transition, have also emerged as a source of friction. Since 2004, Abu Dhabi’s leadership has grown more assertive and less deferential to Riyadh, actively cultivating an independent regional identity. In contrast, Saudi Arabia’s Vision 2030 is explicitly designed to displace Dubai as the region’s primary commercial hub.

What actually breaks?

The UAE is not the first member state to exit OPEC. But what stands out is that all the previous exits were declining producers with little spare capacity, such as Qatar and Ecuador; the Emirates is OPEC’s third largest producer with the largest spare capacity outside Saudi Arabia. Quoting Andy Lipow, President of Lipow Oil Associates, from CNBC[9]: "If countries that are abiding by their quota get disgusted with those that don't, we could see additional exits that could eventually make OPEC irrelevant as a cartel."

The UAE has been effectively the OPEC+’s internal balance against Russia[10], which has regularly overproduced above its quota. This now leaves the KSA alone as the sole force to counter Russian overproduction. The UAE’s strategy[11] of “take the money and run” now brings the oil cartel to a scenario where every other low-cost producer faces the same incentive. This would significantly erode OPEC's main lever of spare capacity to stabilise prices, and the oil cartel might very well be on its path to become yet another large oil producer bloc amongst several others.

The Petrodollar

To start with, the buzz about a possible petroyuan must be taken as mere chatter; yuan slicing does erode dollar monopoly, but only marginally. But the erosion of dollar monopoly cannot be downplayed either, particularly due to an interesting sequence of recent events. On April 23, US Treasury Secretary Scott Bessent’s Senate testimony framed the Fed swap lines as an architecture to prevent dollar dumping by allies under stress[12]. Three days before that, the UAE Central Bank Governor Khaled Mohamed Balama publicly requested a Fed swap line in Washington and told the WSJ that the UAE may have to settle oil in yuan if dollar liquidity tightens[13]. On April 28, the UAE exited OPEC. The exit, in some sense, can be interpreted as Abu Dhabi’s incremental pressure on Washington by signaling it is prepared to hedge towards yuan-denominated settlements.

The shift towards yuan-denominated settlements is not merely rhetorical; the Habshan-Fujairah pipeline[14], which completely bypasses the Strait of Hormuz, for exports to Asia. The possible Murban-yuan settlement, with Murban already offloading at Fujairah[15], would also make INR-denominated oil trade as a credible long-term ask for New Delhi, vis-à-vis oil trade with the UAE and Russia.

The Stakes for India

India is the world’s third-largest oil consumer, and has been able to push non-Hormuz routing from 55% to 70% in recent days[16], largely due to Russian crude via the Red Sea. The UAE exit changes nothing immediately for prices or volumes, and while it sounds painful, the short-term picture is not positive for India. The fundamental reason for that remains the fact that India’s energy security is still tethered to the Strait of Hormuz, through which 30–35% of crude imports continue to transit[17], and the war has led to a sharp decline in the UAE’s actual output, falling to ~2.37 mb/d against an estimated capacity of ~4.3 mb/d[18]. Worse, Indian refiners are now paying $2–8/barrel premiums over Brent[19] for Russian crude, with the US Treasury’s 30-day waiver opening up Russian supply to Japan and other East Asian countries.

In the medium term, the outlook is quite bullish for India. A weakened cartel means weaker price control. For every $10/bbl drop in oil prices, $15-20 billion on India’s annual import bill is saved[20] while increasing its GDP growth[21] by around 0.15% to 0.50%. As the region stabilises, Indian refiners are well-placed to lock in better long-term contracts with the UAE. Murban’s light, low-sulphur grade crude suits Indian refineries, and the delivery point at Fujairah helps bypass Hormuz altogether. Setting the numbers aside, India-UAE is now the single most important Gulf relationship. The India-UAE CEPA, signed in May 2022, has been hugely beneficial, reaching the target of $100 billion in bilateral trade by FY2024-25, 5 years ahead of schedule[22]. The 10-year LNG pact signed in January 2026, for 0.5MMT/yr from 2028[23] also reduced India’s exposure to volatile spot LNG markets. Combined with the rupee-dirham Local Currency Settlement System[24] (LCSS) and the first INR-denominated crude transaction with ADNOC in 2023[25], India stands to benefit in every way possible.

Conclusion

The Emirati exit from OPEC shows the increasingly fragile nature of the GCC, where the member states have diverged in their goals in recent years. The Iran Question has remained the primary fault line when it comes to shaping post-war fragmentation among Gulf states. The UAE has aligned itself with the I2U2 (India-UAE-Israel-USA) and the IMEC, while the KSA, Bahrain and Kuwait have remained more firmly anchored with the American security architecture, and Oman and Qatar have chosen to keep their channels with Tehran open. The US, China and India have also gained from this event. For a long time, the United States has described OPEC as a cartel serving Russian interests[26], and dismantling of the Arab-Russian oil decision unity serves its strategic interests. Oddly, India and China are aligned here; the weakening of the West Asian oil cartel serves their economic interests, with weakened price control and better competition. The cracks in the cartel have always been there, and this OPEC exit might prove to be quite consequential in New Delhi’s energy realignment.

Bibliography

Al Jazeera. "UAE quits OPEC: What that means for the Gulf, energy markets and beyond." April 29, 2026. https://www.aljazeera.com/news/2026/4/29/uae-quits-opec-what-that-means-for-the-gulf-energy-markets-and-beyond.

Al Jazeera Staff and Reuters. "US Treasury Secretary Bessent says Gulf, Asian allies request swap lines." Al Jazeera, April 22, 2026. https://www.aljazeera.com/economy/2026/4/22/us-treasury-secretary-bessent-says-gulf-asian-allies-request-swap-lines.

The Arab Weekly. "India, UAE Sign $3 Billion LNG Deal, Agree to Boost Trade and Defence Ties." January 20, 2026. https://thearabweekly.com/india-uae-sign-3-billion-lng-deal-agree-boost-trade-and-defence-ties.

Axios. "UAE leaves OPEC to pursue 'accelerated' production." April 28, 2026. https://www.axios.com/2026/04/28/uae-leaves-opec.

Bloomberg Economics. "Saudi's fiscal outlook hinges on oil price recovery, production growth, IMF says." World Oil, October 21, 2025. https://www.worldoil.com/news/2025/10/21/saudi-fiscal-outlook-hinges-on-oil-price-recovery-production-growth-imf-says/.

CNBC. "UAE OPEC exit is not without precedent. Who could be next?" April 29, 2026. https://www.cnbc.com/2026/04/29/uae-opec-exit-oil-iran-war.html.

Council on Foreign Relations. "The UAE Announces Exit From OPEC." April 29, 2026. https://www.cfr.org/articles/the-uae-announces-exit-from-opec.

The Diplomat. "Gulf War 3.0: How Is India Securing Its Oil Supplies?" March 16, 2026. https://thediplomat.com/2026/03/gulf-war-3-0-how-is-india-securing-its-oil-supplies/.

Directorate General of Commercial Intelligence and Statistics (DGCI&S). "Insights into Import of Crude Oil and International Crude Oil Prices." October 24, 2025. https://www.dgciskol.gov.in/writereaddata/Downloads/20251024153605Insights%20into%20Import%20of%20Crude%20Oil%20and%20International%20Crude%20Oil%20prices%20.pdf.

Discovery Alert. "India Oil Imports: Supply Risks & Economic Impact." March 13, 2026. https://discoveryalert.com.au/india-oil-imports-impact-economic-framework-2026/

Fortune. "'Take the money and run': Johns Hopkins economist Steve Hanke on why the UAE quit OPEC." April 29, 2026. https://fortune.com/2026/04/29/uae-shock-exit-opec-iran-steve-hanke/.

Fortune. "UAE officials reportedly warned they may be forced to use yuan or other currencies if they run low on dollars amid the Iran war." April 20, 2026. https://fortune.com/2026/04/20/uae-central-bank-dollar-lifeline-fed-treasury-currency-swap-chinese-yuan-iran-war/.

The Guardian. "Biden administration angered by OPEC+ oil output cut." October 5, 2022. https://www.theguardian.com/business/2022/oct/05/biden-administration-angered-by-opec-oil-output-cut.

ICE Futures Abu Dhabi. "Murban Crude Oil Futures." Accessed May 1, 2026. https://www.ice.com/futures-abu-dhabi.

International Energy Agency. "The Oil and Gas Industry in Net Zero Transitions - Executive Summary." 2024. https://www.iea.org/reports/the-oil-and-gas-industry-in-net-zero-transitions.

International Monetary Fund (IMF). "Regional Economic Outlook, Middle East and Central Asia, Statistical Appendix." April 2024. https://www.imf.org/-/media/files/publications/reo/mcd-cca/2024/april/english/statisticalappendix.pdf.

International Monetary Fund (IMF). "Saudi Arabia's Path Forward Amid Lower Oil Prices." December 18, 2025. https://www.imf.org/en/news/articles/2025/12/18/cf-saudi-arabias-path-forward-amid-lower-oil-prices.

The Middle East Insider. "Iran War and Energy Shocks: IMF Revisits India’s Growth Sensitivity." March 14, 2026. https://www.middleeastinsider.com/reports/2026/03/14/imf-india-growth-oil-sensitivity

Ministry of Finance. "Economic Survey 2025-26: State of the Economy and Energy Security." Government of India, January 29, 2026. https://www.eoiparis.gov.in/pdf/economic_survey_2025_26pdf.pdf

Press Information Bureau (PIB). "India-UAE Comprehensive Economic Partnership Agreement (CEPA)." Government of India, May 19, 2023. https://www.pib.gov.in/PressReleasePage.aspx?PRID=1921222

Reserve Bank of India. "Press Release: Local Currency Settlement System between India and UAE." July 15, 2023. https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=56067

Reuters. "India makes first crude oil payment to UAE in Indian rupees." August 14, 2023. https://www.reuters.com/business/energy/india-makes-first-crude-oil-payment-uae-indian-rupees-2023-08-14/

U.S. Energy Information Administration (EIA). "New UAE-based crude oil futures contract introduced in March." August 26, 2021. https://www.eia.gov/todayinenergy/detail.php?id=49316

U.S. Energy Information Administration (EIA). "United Arab Emirates invests to meet 2027 crude oil production capacity goal." 2023. https://www.eia.gov/international/analysis/country/ARE

U.S. Senate Committee on Foreign Relations. "Chairman Menendez Statement on Future of United States-Saudi Relationship." October 10, 2022. https://www.foreign.senate.gov/press/dem/release/chairman-menendez-statement-on-future-of-united-states-saudi-relationship

Disclaimer : Venkatakrishnan Asuri is an undergraduate student at IIT Madras. The views expressed are those of the author and do not reflect the views of the Deccan Centre for International Relations.